Cash-Pay Potential, Insurance Shortcomings

Putting GoodRx and Sesame into a broader context

The previous issue of The Caseload was about GoodRx, and I’m overwhelmed by the number of people that have read or responded to it, especially those who have gotten in touch directly. To all of you: a big, sincere thanks.

Near the end of that last issue, I teased that GoodRx and Sesame have something interesting in common: they’re both making life easier, in small ways, for uninsured patients. GoodRx demonstrates that a great business can be built in the uninsured (or cash-pay) healthcare market; there’s also a case (which I’ll make shortly) that the mainstream system of commercial insurance increasingly misses the mark.

Taking those facts together, I wonder: is there room for a new cash-pay value chain to emerge alongside the existing insurance-based value chain?

In this issue:

The Insurance Bundle and its Shortcomings

Why Insurance Wins Anyway

Success in the Cash-Pay Market Looks Different

How it Happens, and Why it Matters

The Insurance Bundle and its Shortcomings

Let’s start by summarizing the jobs that health plans do, which ones they do well, and where they come up short. There are four main jobs:

Insurance Job #1: Pooling Risk. Most obviously, insurance plans of any kind exist to protect their members from large financial losses, especially related to rare and unpredictable events. Car wrecks, natural disasters, and ER visits all cost more money than most people have on hand at any given time. By collecting a manageable premium each month, insurers smooth out members’ cash flows and guarantee they stay solvent.

For the most part, health plans pool risk effectively, but increasingly fail on the margin. First, premiums increasingly are not manageable, given that the average family spent ~$20k on them in 2018. Second, these high premiums don’t actually remove downside risks for members, as surprise medical bills become more and more common. And finally, cost sharing has increased substantially in recent years, which functionally means that risk is just being passed back to the members. Taken together, these factors make health insurance a worse deal than in the recent past.

Moreover, providers are taking on meaningfully more risk as part of a broader shift forward value-based care. When that happens, the risk pooling function of a payer is correspondingly reduced (because providers bear the financial risk instead). That isn’t necessarily a failure by insurers, but offloading a key part of their value proposition reduces their importance and centrality.

Insurance Job #2: Making Care Decisions. The complexity inherent in medicine creates an information asymmetry problem: patients lack the expertise to determine which care is needed, and which care is superfluous. They need a doctor’s advice to address their illness, but doctors obviously benefit financially from erring on the side of more care (assuming fee-for-service). So, to control costs, patients need help declining unneeded care.

Theoretically, an insurance company can serve that function (e.g. with prior authorizations), and has the right incentive—controlling costs—to keep doctors in check.

The counterargument to that theory is that patients all have different preferences and risk tolerances, and also that doctors’ clinical assessments are highly nuanced, often uncertain, and situation-specific. Individualism and nuance are necessarily lost in the prior authorization process, so it’s reasonable to believe that many health outcomes could be improved by keeping the decision making power (which is inextricable from financial risk) with the patient. As I’ve written in the past, the prior authorization process diminishes the customer experience.

A quick example: Assume patients A and B have the same diagnosis. A wants to try the latest, most expensive, and risky procedures to cure a given illness, while B is skeptical and prefers less treatment. If these patients work for the same employer, they’re probably on the same plan, pay the same amount, and even receive the same care, despite their vastly different preferences.

Removing the insurer from the decision, though, increases moral hazard, which limits the insurer’s ability to cost-effectively pool risk, which in turn is why this job typically comes bundled with risk pooling. But it’s an awkward fit. Moral hazard can be reduced by implementing cost sharing measures (like high deductibles and coinsurance), but as noted above, those just push risk back onto members and reduce the overall value of the product.

Insurance Job #3: Negotiating Prices. Insurance plans strike non-public pricing deals with providers (and pharmacies, via PBMs). Again speaking theoretically, this helps members because the plan can negotiate on behalf of many members at once. While a single patient can’t possibly know the going rate for untold types of procedures, insurance plans can and do. Plus, patients are often too sick at the point of care to negotiate prices on their own.

On the other hand, plans don’t have much incentive to negotiate low rates with providers. That results in occasional situations where it’s actually cheaper to not have insurance; edge cases to be sure, but suggestive that insurers aren’t using their market power to achieve low prices. The evidence that insurers reduce costs for their members seems mixed.

Insurance Job #4: A Substitute for Debt. Outside of healthcare, large expenses that are predictable are usually financed by a combination of savings and debt. Examples include cars, college educations, home appliances, and so on.

Lots of predictable expenses exist in healthcare, too (e.g. chronic care management, some joint surgeries), but they’re paid for with insurance, rather than debt. Insurance is designed to deal with unpredictable events (all those actuaries and claims processors add overhead), so it’s more expensive than debt when it comes to financing predictable care. This is a job that insurance simply isn’t cut out for, but it gets bundled in anyway. And note that this makes the Job #1 (risk pooling) much easier on insurance companies: if many of your claims are actually completely predictable, pooling risk is not just trivial, it’s unnecessary.

Compared to filing an insurance claim, it might seem like a bad outcome for patients to go into debt over a medical expense. However, the main difference between debt and insurance is the timing of the payments: with debt, patients owe a steady stream of payments after the service is provided; with insurance, the payments are owed in advance. (In both cases, there is also an interest payment—with debt it’s made explicit; with insurance, plans collect interest on the float.)

Even so, insurance does not seem to keep people from getting into medical debt. Gains in coverage following the passage of the ACA coincided with an increases in the proportion of bankruptcies driven by medical expenses.

The main takeaway from examining these jobs is that we demand a lot of our insurance plans, and in trying to accomplish everything, the plans come up short.

Why Insurance Wins Anyway

For all of the problems with traditional health insurance, only around 10% of Americans go without. There are two big reasons for that.

First, the regulatory environment strongly favors insurance. On the employer side, tax rules mean that employers can provide health insurance with pre-tax money, and workers expect employer healthcare in lieu of higher, but taxable, wages. That’s because the alternative would be to buy private insurance with post-tax money. Additionally, companies with over 50 employees are required to offer coverage.

Outside of the employer market (and setting aside Medicare and Medicaid for now), there’s the individual ACA market. There’s no tax deduction here, but the ACA itself subsidizes low-income patients’ insurance, meaning that their cheapest route to healthcare access is also through insurance.

(Quick aside, one angle on the ACA is as a subsidy to insurance companies: anyone who couldn’t afford insurance is given a mandate + cash to go buy insurance, which means the final result is…more cash for insurance companies. Said differently, the ACA increases total spending on health insurance in order to make health insurance more affordable to low-income buyers. It uses insurance as a vehicle for economic redistribution, but that doesn’t mean it achieves, or even tries to achieve, lower spending in aggregate. Also N.B., I mostly like the ACA.)

The second reason most people get insurance is that the healthcare system is hard to access and navigate without it. Interestingly, that difficulty is a function of the extent to which the system is built for people with insurance. For example, cash-pay patients depend on transparent pricing to get a fair deal. However, hospital systems and pharmacies rarely publish prices, because people with insurance don’t need to see them. A general feedback loop emerges, which is that as more people have insurance, the system increasingly can neglect those without it, which in turn encourages more people to sign up for insurance.

This is why I’ve been so struck by both Sesame and GoodRx, and why I’ve focused on them for recent essays. Both companies are focused on addressing the needs of patients outside of the dominant insurance system, and by doing so, they’re making it easier to be uninsured.

If you believe in the power of the insurance lock-in feedback loop mentioned above, that positioning begs further examination. On the other hand, if you’re really ambitious and trying to disrupt the system, you need an attack vector from an angle that’s orthogonal to everyone else’s. And the best place to build a business with high upside is generally not in the part of the market where needs are broadly satisfied; change is likeliest where things suck the most.

Let me state it plainly: the underserved cash-pay market is a wedge for broad disruption an insurance-based ecosystem that is failing patients on multiple fronts, but has few apparent vulnerabilities.

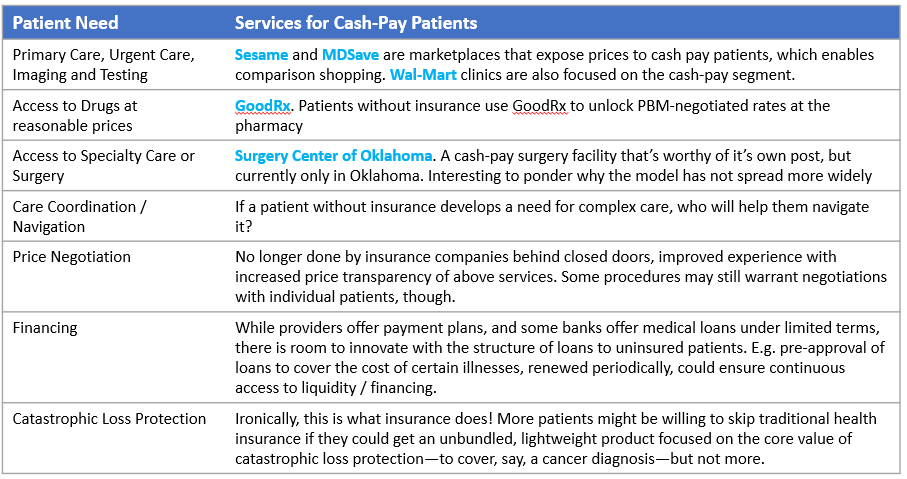

Success in the Cash Pay Market Looks Different

The needs of uninsured/cash pay patients are different than those with insurance. Here’s a quick sketch of some of those needs; it’s apparent there are some gaps.

(Readers, what have I missed?)

The development of the cash-pay market, if it happens, won’t be linear: there is a kind of feedback loop where each additional need that gets addressed enables the ecosystem to address the needs of more and more patients, which then de-risks further investment in the ecosystem broadly. Starting a flywheel like that is notoriously difficult; the recent success of GoodRx provides some reason for optimism.

Going to market in the cash-pay segment is also hard: insurance companies have an established sales channel (employers) that doesn’t exist for cash-pay consumers. As I’ve written, GoodRx has succeeded in part by selling through doctors, but centralized sales channels are scarce, and the default ones (Google and Facebook) are expensive.

Further complicating the picture is that not all cash-pay patients are the same, or have the same needs. Some might be financially stable, but decide against insurance because they’re young and healthy. Others might be low-income immigrants who are unable to get Medicaid coverage that they would technically qualify for. The more fragmented the customer needs become, the harder it is to meet them all.

The reward for businesses that tackle these challenges is an eventual seat at the table of the mainstream healthcare market, without having to directly challenge behemoths like United, CVS, and Cigna.

How it Happens, and Why it Matters

It remains to be seen if the cash-pay ecosystem can mature enough to provide an experience that’s “good enough” for most consumers. To gain adoption, it will need to be better than the traditional insurance market on at least a few dimensions. Let’s assume, for the sake of a thought experiment, that it gets there.

This would likely trigger a migration of some marginal customers who are especially poorly served by insurance, relative to the improved cash-pay experience. Those marginal customers are likely to be younger and healthier than the rest, so their defections would drive up premiums, triggering more defections. I don’t think this cycle continues forever—regulations lock in insurance, and insurance plans can cut prices—but it does expand the cash-pay market from where it sits now.

Small employers would have the option to unbundle insurance from employment, possibly by offering higher salaries to workers, who can use the money to get care through the new value chain. Large employers can’t do this though; again, they’re required by the ACA to offer insurance.

That leaves providers, who would gain from less burdensome interfacing with insurance plans (e.g. fewer prior auths). On the other hand, they still need to address insurance plans for some customers, and so maintain the overhead to do so (billing consultants and the like), while also putting more resources into the expanded cash-pay channel. While providers are used to selling to insurance companies, they’ll have to re-orient to also sell to cash-pay patients, a tall ask.

For the healthcare system as a whole, maybe the biggest question is whether a cash-pay ecosystem would lower the cost of care. I think there’s reason to be hopeful: end consumers that can compare prices are a powerful mechanism for regulating costs. But supposing it doesn’t? Consumers will return to their insurance plans. From that standpoint, the cash-pay ecosystem represents a call option on a better healthcare system: great if it works, but otherwise no harm done. It’s part of a portfolio of approaches that the healthcare system is taking to reduce costs, alongside ideas like provider risk bearing, or digital tools that increase patient engagement.

Bonus

I got beaten to the punch by Nikhil Krishnan at Out of Pocket this week. He’s got a great post on price transparency that touches on some of the same themes, and he’s always worth a read. (Link)